Let me tell you something that drives me crazy. People will spend three hours comparing TVs on Black Friday but won’t spend twenty minutes comparing mortgage rates before they sign for a 30-year loan. And then they wonder why they feel house-poor a year later.

Girl. The interest rate on your mortgage is one of the biggest financial decisions you will ever make. A difference of half a percent can mean tens of thousands of dollars over the life of the loan. So let’s talk about how to actually shop rates the smart way — with the right tools.

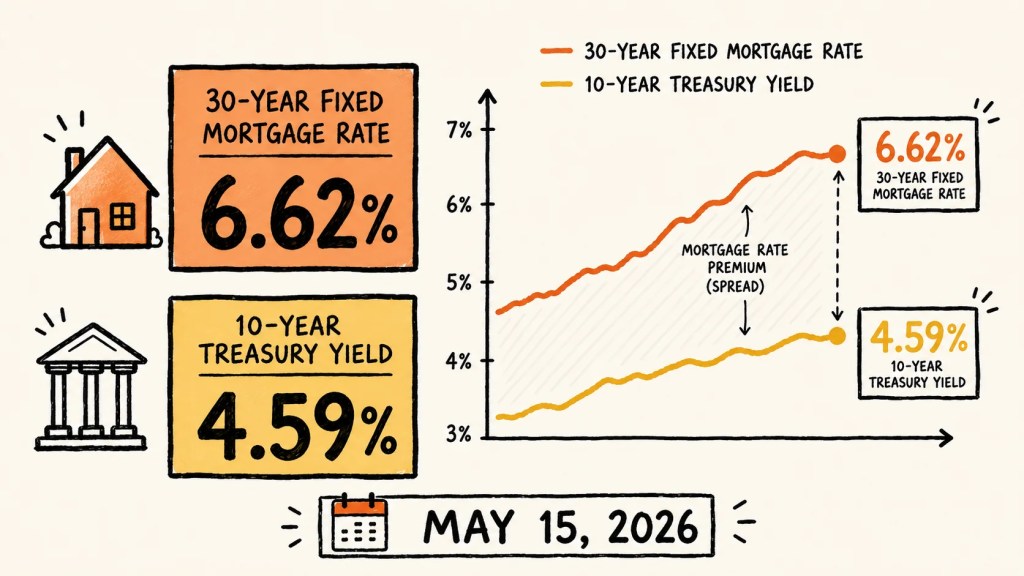

Image Credit: BytePith

Why mortgage rates aren’t all the same

Quick reality check. The rate you see on TV or in a Google ad is not necessarily the rate you’ll get. Your actual rate depends on your credit score, your down payment, the loan type, the property type, where you live, and which lender you go with. That’s why comparing is everything.

And here’s the thing nobody talks about: lenders compete for your business. If you walk in with quotes from other lenders, they will often beat them. But you have to do the legwork to get those quotes in the first place.

The best mortgage rate comparison tools

1. Bankrate

Bankrate has been the go-to for rate comparisons forever, and it’s still one of the best. Their daily rate tables let you see what’s happening nationally, and you can filter by loan type — 30-year fixed, 15-year fixed, FHA, VA, jumbo, ARM. They also pull from multiple lenders so you’re not stuck looking at one bank’s marketing.

Best for: getting a snapshot of where the market is today.

2. NerdWallet

NerdWallet’s mortgage tool is great because it gives you personalized rate estimates based on your credit profile and loan info. It’s less of a “here’s the average” tool and more of a “here’s what you would actually get.” Their lender reviews are honest and helpful too.

Best for: figuring out which lender to actually call.

3. Zillow Mortgage Marketplace

Zillow lets you request quotes from multiple lenders without giving up your phone number to twelve different companies (which… we’ve all been there). You fill out a short form and get matched. The lenders compete for you.

Best for: introverts who’d rather not field a million sales calls.

4. LendingTree

LendingTree’s whole model is letting lenders compete for you. You fill out one application, and up to five lenders send you rate offers. Be ready for some phone calls, but the rates are often very competitive.

Best for: people who want to play lenders against each other (in a healthy way).

5. Mortgage News Daily

This one’s not a comparison shop — it’s where I send people who want to actually understand what’s happening with rates. They publish daily updates and analysis, and reading them for a week will teach you more about how rates move than any commercial will.

Best for: nerds, planners, and anyone tired of the “rates are dropping!” headlines.

6. Freddie Mac’s Primary Mortgage Market Survey

Want to know the actual national average for a 30-year fixed mortgage rate this week? Freddie Mac publishes it every Thursday. Free, no fluff, no marketing.

Best for: a baseline truth-check before any lender quote.

7. Your local lender or credit union

I always tell my buyers to get at least one quote from a small local lender or credit union in addition to the online options. They often beat the big banks on rate, and they actually know our area. A loan officer here in the Susquehanna Valley who works with first-time buyers and rural properties is going to understand things a national call center never will.

How to actually compare rates (the right way)

Here’s where most people mess up. They look at the rate and only the rate. But the rate is just one piece. You also have to look at:

The APR (annual percentage rate), which includes fees and gives you the true cost of borrowing. The closing costs and any lender fees. Discount points — are you paying upfront to lower your rate? Is that worth it for how long you’ll stay in the home? The type of loan — is it fixed or adjustable, conventional or FHA? Lender reputation and how easy they are to actually work with.

A loan with a slightly higher rate but $4,000 less in fees might save you more money than the “lower” rate option.

The smart shopping process

Step one: pull your credit and know your score. You don’t need a mortgage broker to do this — Credit Karma, Experian, or your bank’s app will show you.

Step two: get rate quotes from at least three lenders within a 14-day window. That’s important. Multiple mortgage inquiries inside a 14-day window count as one credit pull, so it won’t hurt your score.

Step three: ask each lender for a Loan Estimate. This is a standardized form, federally required, that shows you the rate, the APR, the monthly payment, and all the fees. It’s the only way to compare apples to apples.

Step four: don’t pick based on rate alone. Pick based on total cost, who you trust, and who actually returns your calls.

A word about online-only lenders

Online lenders like Rocket Mortgage and Better.com can have great rates, but they can also have less hand-holding. If you’re a first-time buyer or you have a complex situation (self-employed, rural property, unusual income), I’d lean toward a lender who’s actually going to pick up the phone when you have a question at 8pm on a Tuesday.

There’s nothing wrong with online lenders. But cheaper isn’t always better when you’re talking about the biggest purchase of your life.

Don’t let rates scare you into renting

Last thing. I see this so much: someone hears rates are higher than they were two years ago, and they decide to wait. Then a year passes, rents go up, home prices go up, and they’ve lost more money waiting than they would’ve paid in interest.

You don’t marry your interest rate. You can refinance later. But you can’t go back and recover the money you handed your landlord while you waited for the “perfect” market.

I’m not telling you to buy if you’re not ready. I’m telling you to know your numbers.

Let’s compare your real options

If you want help walking through what your actual mortgage payment could look like — or which local lenders I’d recommend in the Susquehanna Valley — I’ve got you. I work with a few I really trust, and I’ll never push you toward someone just because they pay me a referral fee (because I don’t take any).

What’s the one thing about mortgage rates that’s been holding you back from starting this process? Send me a message — let’s get you real answers.

Leave a comment